The COVID-19 pandemic and resulting restrictions on domestic and international travel, economic activity, and individual movement are having an unprecedented impact on the lodging and tourism industry in Latin America and worldwide. While government authorities across the region work to manage restrictions and phased reopening plans, uncertainty prevails over the duration of the global pandemic. What started as a health crisis with tragic consequences for victims of COVID-19 morphed over the course of the year into a deep economic downturn. While the pandemic is not yet under control, therapeutics have improved, and different vaccines seem to be closer at hand.

The COVID-19 pandemic and resulting restrictions on domestic and international travel, economic activity, and individual movement are having an unprecedented impact on the lodging and tourism industry in Latin America and worldwide. While government authorities across the region work to manage restrictions and phased reopening plans, uncertainty prevails over the duration of the global pandemic. What started as a health crisis with tragic consequences for victims of COVID-19 morphed over the course of the year into a deep economic downturn. While the pandemic is not yet under control, therapeutics have improved, and different vaccines seem to be closer at hand.The breadth and depth of the pandemic crisis are unquestionable. However, it is good to step back to evaluate factors that may have a bearing on a recovery period and on the performance of the hotel industry beyond the present time. In this article, we seek to outline the fundamental elements and drivers of different Latin American hotel markets in the hope that this may serve hotel owners, lenders, operators, and other market participants in gaining perspective that, in turn, may be of value in decision-making processes.

Mexico Overview and Outlook

Hotel Industry Structure

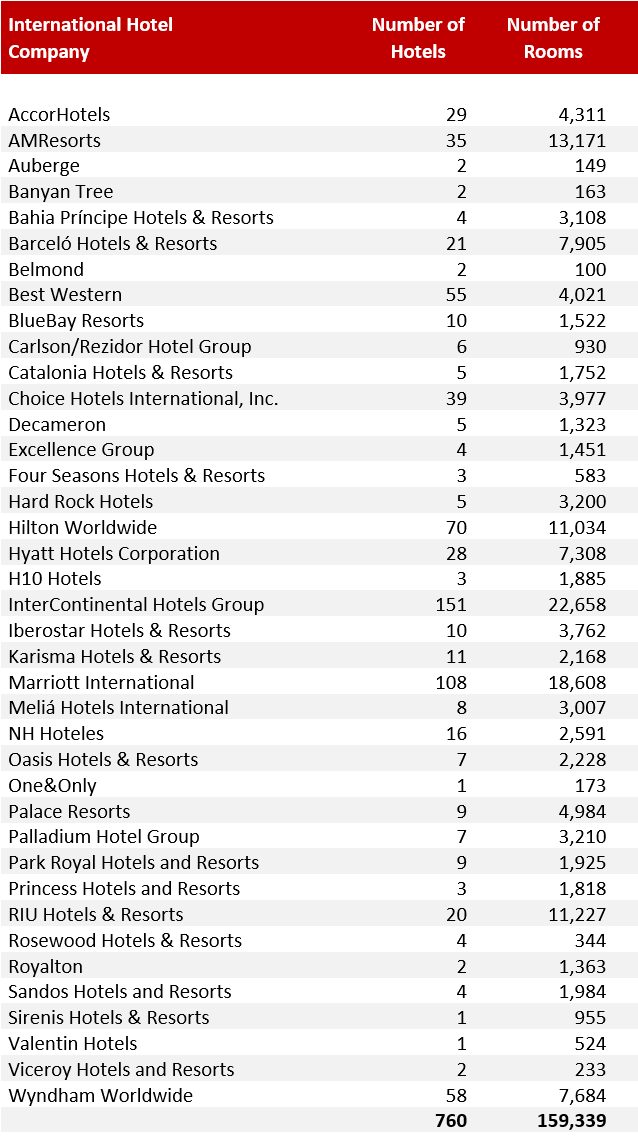

Our overview of the current state of the Mexico hotel market begins with a short primer on the structure and key drivers of its lodging industry. Mexico is a country of 126 million inhabitants with a relatively large and diversified economy. Unlike many countries, Mexico’s lodging industry is split between robust business and leisure-oriented sectors, and this turns out to a considerable strength. Furthermore, Mexico has long-established national and regional brands, as well as extensive international brand footprints, which gives Mexico considerable capacity and distribution.Exhibit 1: Chain Representation - Mexico

Source: HVS

Source: HVS

Business Lodging Drivers and Market Performance

With the introduction of the North American Free Trade Agreement (“NAFTA”) in January 1994, Mexico’s economy began a transition from high dependence on oil exports, which had previously totaled over 60% of total exports, to an export manufacturing economy. Over the past 26 years, the country has experienced considerable growth in the automotive, aerospace, home appliances, and electronics sectors, among others. As a result, the economy is roughly three times the size of pre-NAFTA, and oil exports now account for less than 10% of the total.

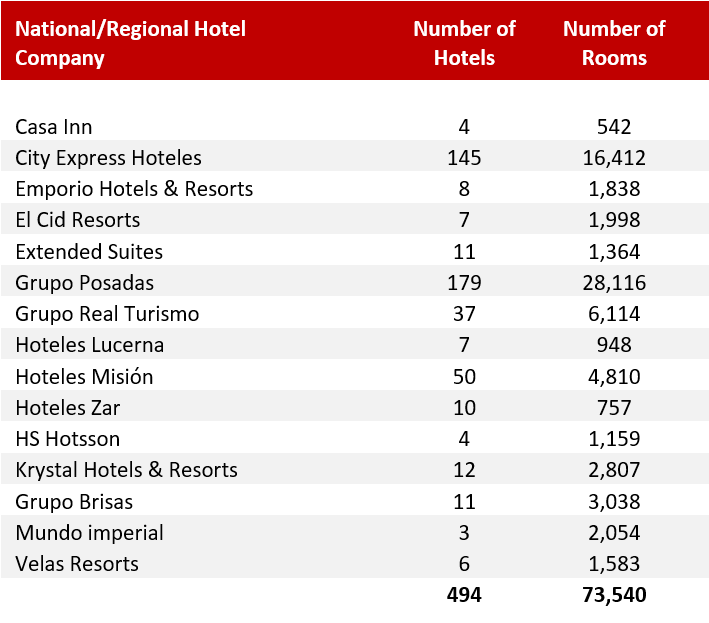

The greatest concentration of business-focused lodging is present in Mexico’s three largest cities, namely, Mexico City, Guadalajara, and Monterrey, and in some 20 mid-sized cities, mostly in central and northern Mexico. Central Mexico is generally considered to extend roughly from Puebla to Aguascalientes, passing through Mexico City and including the cities of Queretaro and León. Northern Mexico runs along the U.S.-Mexico border states, including the cities of Tijuana, Ciudad Juárez, Chihuahua, Monterrey, Saltillo, and Reynosa, among others. Over the past ten years or so, national and international hotel chains have expanded their footprints, capturing demand growth spurred by industrial growth. This development has been accompanied by evolving real estate capital markets, including the creation of FIBRAs (the Mexican version of REITs) and other investment vehicles, as well as access to a growing number of sources of debt.

Exhibit 2: Mexico Branding Trends

Source: HVS

Source: HVS

Most of the country’s business-focused hotels initially closed as result of COVID-19 and as the nation’s economy halted, similar to other parts of the world. A gradual reopening of hotels began in June and July, primarily in the central and northern parts of the country, as portions of the economy were slowly reactivated—in many cases mirroring the reopening of key business sectors in the United States. In fact, in the post-NAFTA era, it is virtually impossible to assemble a car in either the U.S. or Mexico without access to component parts from an integrated cross-border supply chain. Through the summer and into the early fall, hotels have had government limitations on the percentage of rooms that can be opened, generally around 30% of inventory, allowing for occupancies around 20% in most markets. However, a slow build-up of business demand related to export manufacturing has commenced, as essential domestic and international business travel is occurring to carry out roles that cannot be completed remotely.

In contrast, higher-level executives are not yet traveling in major cities within the upper-upscale segment. Flight paths from main feeder markets are slowly being reestablished, but multinational companies have opted to wait for resolution of travel restrictions, electing not to put executives at risk. Also, given the current economic conditions, travel budgets have been curtailed. As elsewhere, group and incentive business travel have largely been shut down, as events have been rescheduled and postponed to next year.

A renewed version of NAFTA known as the U.S., Mexico, and Canada Agreement (USMCA) went into effect July 1, 2020, which should provide stability for mid-term business and manufacturing growth. Many companies are seeking to expand or establish a presence in Mexico, due in part to supply-chain interruptions in Asia, in some cases brought on by recurring tension in China-U.S. trade relations. The López Obrador administration maintains an anti-business rhetoric and has taken a certain specific actions that create uncertainty, notably, the cancellation of a partially built new airport to serve Mexico City, the cancellation of an advanced beer-manufacturing plant in Mexicali, and renegotiation of different agreements with international participants in Mexico’s energy sector. However, regarding foreign trade, which is the underpinning for Mexico’s economic stability, Mexico’s administration has proved to understand the strategic importance of USMCA and has fully supported its enactment and implementation. Furthermore, while business leaders justifiably regret that Mexico has provided virtually no fiscal stimulus through the COVID-19 pandemic, the government has shown a commitment to long-term fiscal discipline that will tend to serve the country well as the economy reactivates.

Leisure Lodging Drivers and Market Performance

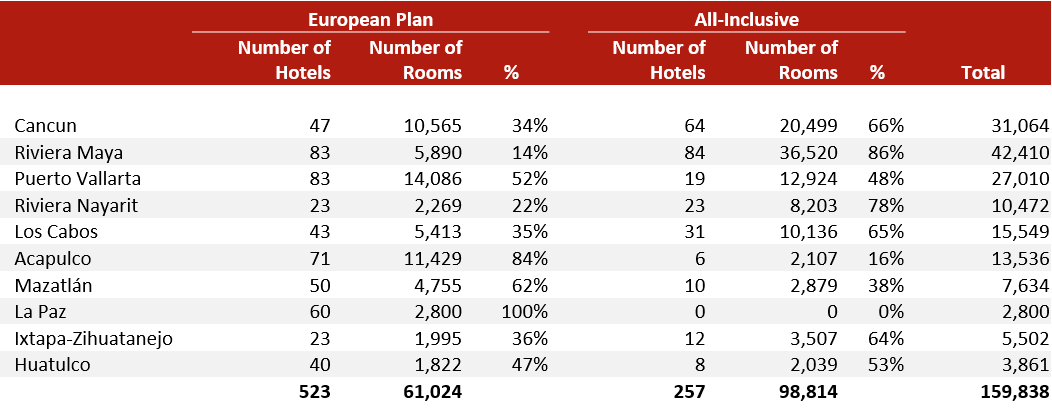

Mexico’s leisure segment is anchored by beautiful destinations and popular beaches. The country’s cultural heritage brings visitation to the country, and its resorts are known for high-quality service. The quality of Mexico’s hotel inventory and the presence of a vast array of operators and brands are important attributes, with urban and beach destinations alike featuring lodging experiences along the entire market spectrum, from luxury product to innovative economic concepts. The country’s key vacation destinations include the Cancún-Riviera Maya Corridor and Los Cabos, as well as the Puerto Vallarta-Riviera Nayarit Corridor. Several up-and-coming markets, including Huatulco, La Paz, and Mazatlán, provide additional alternatives and seek to take steps that may lead to their full consolidation. Mexico’s proximity to the U.S. and Canada is highly favorable for the sector, with many travelers being familiar with the country’s primary leisure destinations. This popularity has driven the establishment of many air routes to Mexico from cities such as Los Angeles, Houston, Dallas, Miami, New York City, and Chicago, among many others. Certain markets also enjoy significant visitation from European and South American visitors, and the potential positioning of Mexico’s destinations in Asia remains a long-term goal.An interesting aspect of Mexico’s vacation travel sector is that hotel supply is split between traditional European Plan (EP) properties and a robust offering of all-inclusive properties. These tend to be complementary in nature, and the market has proven to accept both formats over the years. Furthermore, Mexico has an established track record in execution of highly attractive master-planned projects, often featuring a layered approach to hotel supply, along with variety of residential product.

Exhibit 3: Four- and Five-Star Hotel Supply

Source: SECTUR, HVS

Source: SECTUR, HVS

This strong industry remains fragmented. Federal government support for the industry is limited and the cancellation of a national public-private tourism promotion agency at the start of the López Obrador administration has presented and unwelcome challenge. At the same time, in all destinations, the trend is for greater organization and cooperation between local authorities and private-sector players to address different tasks and challenges, including security, infrastructure development, tourism promotion, and more. A key element of risk revolves around security issues and the perception that they impact tourist destinations. While key resort areas are safe and distanced from the areas in which criminal activity is more prevalent, the occasional incident and a broader perception of unsafe conditions remain an issue of constant concern.

Resorts shut down for COVID-19 and ultimately missed out on part of the country’s high season, including Easter week. Also, the summer season was largely a loss. A gradual reopening of resorts began during the summer and early fall, along with the gradual reopening of flight paths, some domestic and some international. Foreign tourist arrivals to Mexico were down 58.7% year-to-date through August 2020, according to Mexico’s tourism ministry, SECTUR. U.S. tourist arrivals, which make up most foreign arrivals, were down 55.3% for the same period. Like urban locations, resort destinations have government limitations on the percentage of rooms that can be opened, in most areas, currently at 30% of inventory. Accordingly, resort destinations have had to rely on domestic travel this year, as international travel has been affected by travel restrictions and limited airlift. In addition, incentive business to Mexico has been largely canceled for the year. As the winter season approaches, owners, operators, and wholesalers report a clear uptick in bookings, both domestic and international. As in other countries, safety protocols have been implemented to mitigate exposure to COVID-19. Still, as the pandemic resurges in the U.S., it will be important to follow travel trends through the coming months.

Investment Environment and Outlook

Contact with investors, lenders, and market participants reflects that Mexico’s hotel investment market is behaving similarly to what is being experienced in the U.S., and if possible, parties are avoiding hotel transactions. However, based on the valuation exercises that we have performed, value declines can currently be expected in the 15–25% range, depending on asset and location. Based on an anticipated recovery and looking beyond the immediate short-term to a more normalized/stabilized period, projects are expected to close the gap between pre-pandemic and mid-pandemic variances in value.A review of Mexico’s active development pipeline reflects that completion of new supply is largely being delayed, as developers are slowing down delivery processes by up to twelve months, aiming to open assets in a somewhat better market. While projects that had secured financing prior to the pandemic are advancing, many yet-to-be funded projects in the pipeline will have to be reevaluated.

Our opinion of the Mexican hospitality industry is that it comprises robust business and leisure segments. All are experiencing declines now due to COVID-19. However, the industry is structurally sound and well positioned in the mid- to long-term. We expect improved occupancy and average rate (ADR) performance through 2021, with a prolonged overall recovery through the year 2023.

Central America Overview and Outlook

Central America consists of seven countries of varying sizes and characteristics; thus, the regional hotel industry is both relatively small and fragmented. Belize has a small population of approximately 400,000, while the other six countries reflect population ranges between 4.3 million for Panama and 17.9 million for Guatemala. Most economies are driven by local demand and small manufacturing bases; some agricultural exports exist and, of course, Panama has its canal. Tourism has the greatest relative weight in Belize and Panama, as well as Costa Rica with Guanacaste’s beach area and the country’s jungle areas that normally drive significant levels of nature tourism. The recent openings and the development of different internationally branded EP and all-inclusive hotels should support demand growth in Guanacaste and further define the destination, bringing a more varied product offering and additional airlift. Two countries with relatively good air connectivity, Panama and El Salvador, have a base of regional group business that will likely remain shut down in the current COVID-19 environment but that should gradually recover.As in other parts of the world, travel is down and will depend on recovery in U.S., as well as air travel, to bounce back. The first half of 2021 is anticipated to remain very sluggish for markets such as Costa Rica, with demand expected to ramp up after the spring. Generally, Central America (and much of the Caribbean) have experienced the largest percentage and longest duration of hotel closures, compared to other markets such as Mexico, the U.S., and Puerto Rico. Travel restrictions are slowly loosening, but this varies by country.

South America Overview and Outlook

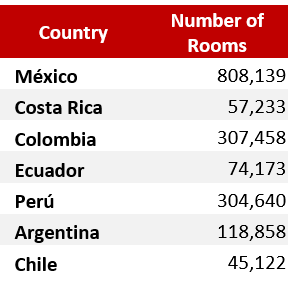

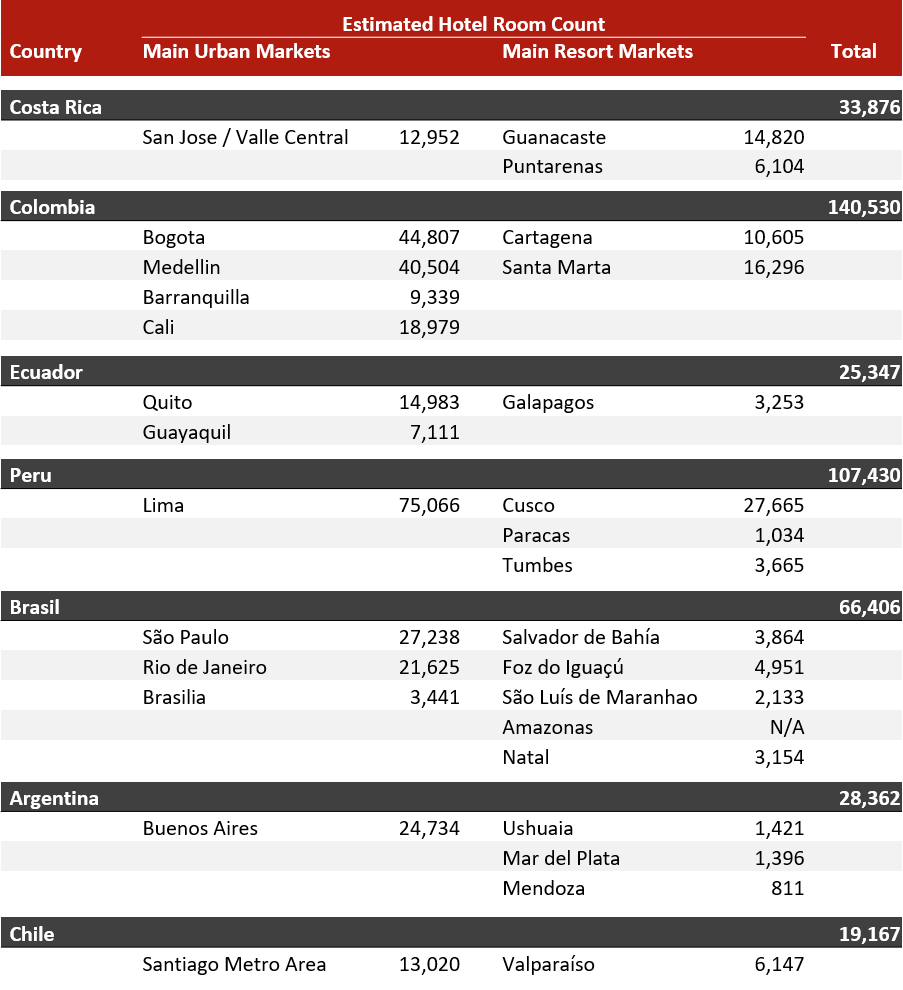

South America comprises twelve very different countries; thus, hotel markets vary per country. While the populations in Guyana and French Guinea are small, the four countries that primarily drive the continent’s economic activity are Chile (population 19 million), Colombia (51 million), Peru (33 million), and Brazil (213 million). In certain larger countries, such as Peru, economies are driven to a considerable extent by commodity industries such as mining. Other economies, including that of Ecuador, are more oriented toward agriculture. Meanwhile, Argentina, Chile, Colombia, and Brazil, in varying degrees, have more diversified economies, including more significant manufacturing sectors.Exhibit 4: Number of Rooms by Country

Source: HVS, DATATUR, MINCETUR, REPORTUR, SERNATUR – 2019

Exhibit 5: Selected Inventory by Country

Source: HVS, DATATUR, MINCETUR, REPORTUR, SERNATUR – 2019

Exhibit 5: Selected Inventory by Country

Source: HVS

Our analysis of different markets across Latin America bears out that those driven by manufacturing and, particularly, export manufacturing, tend to generate deeper demand than those more dependent on mining and agriculture. As such, the nature of hotel inventories and industry performance varies greatly by country.

As has been documented in the news since the start of the COVID-19 pandemic, South America has been deeply affected, with the hotel industry in several regions having shut down almost entirely. While variations exist in each country’s approach to management of health and economic challenges, conditions are difficult throughout. In Colombia, with a focus on Bogota, hotel reopenings are just now occurring. El Dorado International Airport is typically the third-busiest airport in Latin America but remained closed to commercial aviation from March through much of August. Leisure transient demand to Cartagena has similarly been severely affected. Peru remains largely shut down to travel, with Lima’s international airport scheduled to resume activity in November. In Brazil, a sizeable local economy remains sluggish, but international travel is limited and may come to impact the high season, particularly around Carnival festivities. Chile’s recovery is similarly slow, but the country’s strong economic underpinnings should allow for a somewhat better recovery. In Argentina, with a focus on Buenos Aires, hotels closed mid-March and were allowed to reopen in October. International flights resumed as of September, but the anticipation is that international airlift demand will not pick up right away. The pharmaceutical industry has historically been an important generator of both corporate transient and group demand, and the recent announcement regarding Astra Zeneca’s COVID-19 vaccine, to be produced in Argentina, has elicited an optimistic outlook for the near future.

The outlook for South American countries is presently guarded. If health conditions can reasonably be brought under control, countries with more diversified economies are likely to see a gradual rebuilding of business demand. Meanwhile, in the southern hemisphere, the summer season (between November and April) presents an important opportunity to attract some visitation, particularly in the leisure segment. As in other parts of the world, a shift to more normalized conditions is expected to begin during 2021 and to evolve as economic conditions improve.

About HVS

HVS, the world’s leading consulting and services organization focused on the hotel, mixed-use, shared ownership, gaming, and leisure industries, celebrates its 40th anniversary in 2020. Established in 1980, the company performs 4,500+ assignments each year for hotel and real estate owners, operators, and developers worldwide. HVS principals are regarded as the leading experts in their respective regions of the globe. Through a network of more than 45 offices and more than 500 professionals, HVS provides an unparalleled range of complementary services for the hospitality industry. From Mexico City, HVS serves clients throughout Mexico, as well as Central and South America. For more information, please visit our website.

HotelExecutive.com retains the copyright to the articles published in the Hotel Business Review. Articles cannot be republished without prior written consent by HotelExecutive.com.

About Richard J. Katzman

0 Comments

Success

It will be displayed once approved by an administrator.

Thank you.

Error