Owing to its rich cultural heritage, prestigious educational institutions and wide range of attractions across fashion, media and sports, London is a key destination for international visitors. In addition, its strong influence as a financial centre and a hub for technology and innovation defines it as a leading market in terms of hospitality and hotel investment. Despite its size, London’s accessibility through various international airports as well as the Eurostar high-speed rail service facilitates travel, ensuring a steady influx of both leisure and business travellers. These factors are expected to drive London’s continued success as a leading global tourism destination, even in the face of economic challenges and geopolitical uncertainties.

Source: HVS Research

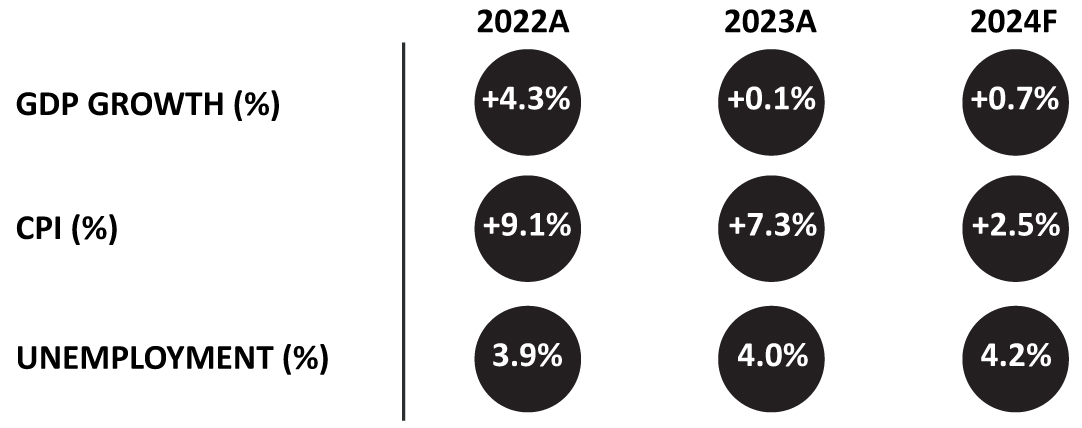

Economic Indicators – UK

Source: IMF

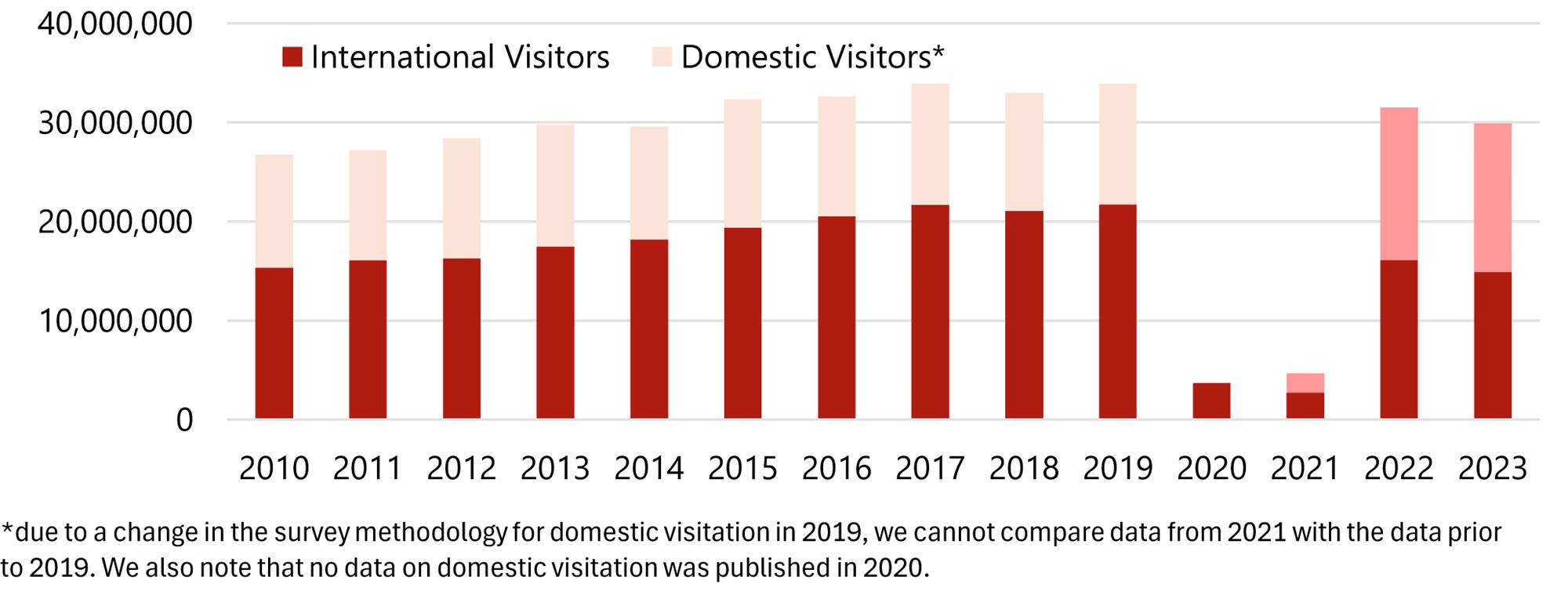

Tourism Demand

Years of practically uninterrupted growth delivered close to 34 million visitors to London in 2019, mainly driven by international demand which increased its share from less than 60% in 2011 to around 64% by 2019. In 2020, global tourism was halted by COVID-19, causing London’s international visitation to plummet by more than 80% to 3.7 million. Both 2020 and 2021 witnessed significant challenges owing to COVID-19 containment measures; however, in 2022, international visits notably increased to 16.1 million, 75% of 2019 levels.

In 2023, visitation declined by 5% compared to 2022, with both international and domestic figures decreasing over that period. That could be explained by factors such as the necessity for foreigners to apply for a visa since Brexit or the cost-of-living crisis. Additionally, major events in London during 2022, such as Queen Elizabeth’s Jubilee, the UEFA Women’s Euro final, the first Notting Hill Carnival post-pandemic, and Queen Elizabeth’s funeral, contributed to high visitation figures that year. Consequently, the drop in 2023 could reflect a natural readjustment following the high levels of visitation in 2022.

We note, however, that Visit Britain is confident in the UK’s ability to return to 2019 levels of visitation. In 2019 the UK welcomed 40.9 million inbound visits before substantially decreasing during COVID. In 2022, visits had recovered to 31.2 million, and the latest inbound forecast for 2024 (made in May 2024) was for 38.7 million visits, 95% of 2019 levels.

International Visitation Still Lagging Behind Pre-Pandemic Levels

Source: HVS Research

Hotel Performance

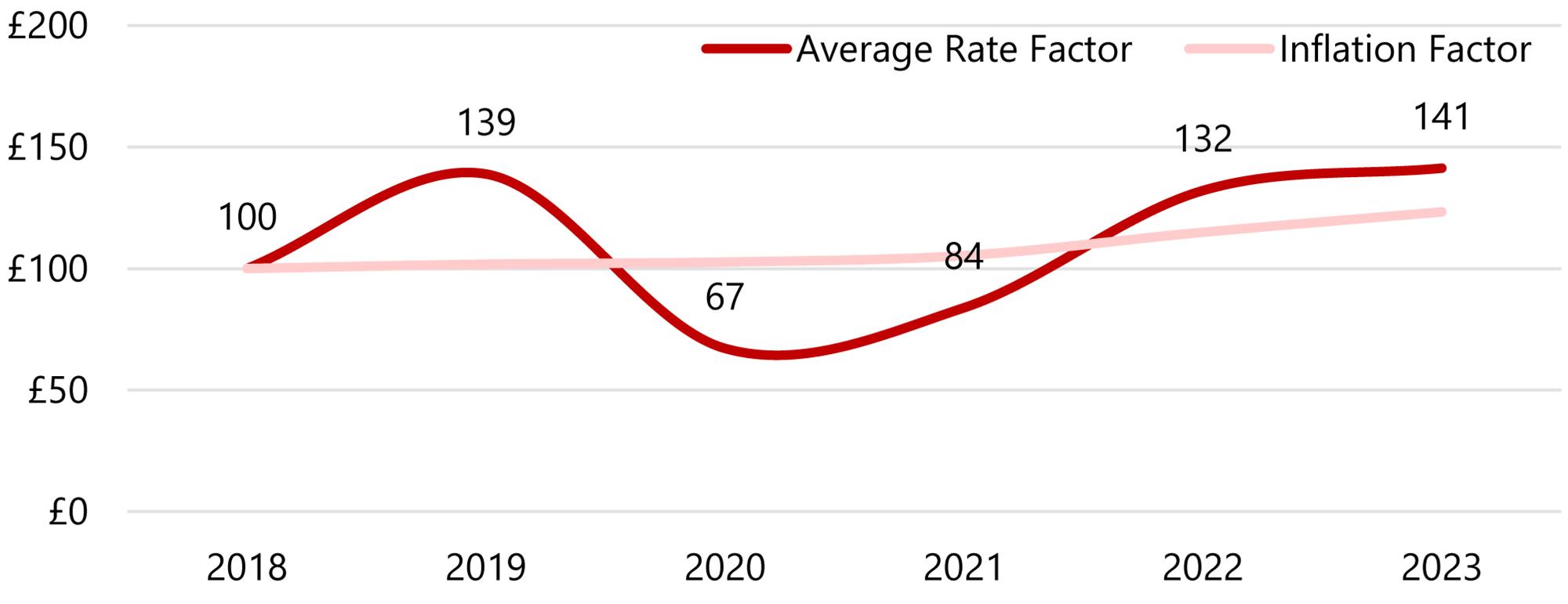

- Hotel performance rebounded strongly post-COVID-19, with steady growth in occupancy, average rate, and RevPAR from 2021 to 2023.

- Average rate and RevPAR notably increased in 2022 and 2023, eventually surpassing pre-pandemic levels.

Average Rates Growing Above Inflation

Source: HVS Research

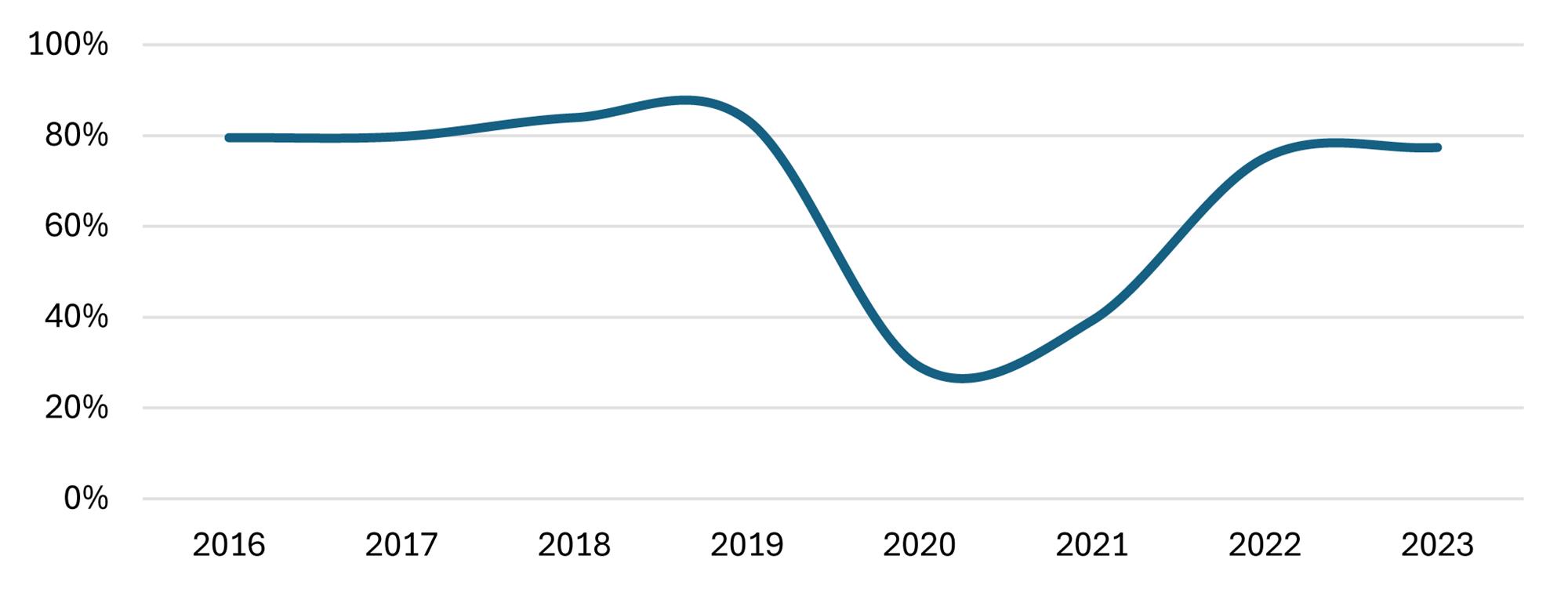

- Occupancy rates surged in 2022, reaching 75% from 39% in 2021, and increased by a further 2% in 2023. However, the occupancy in 2023 still lagged some 3% behind 2019 levels.

Occupancy Still Recovering

Source: HVS Research

- Year-to-August 2024 RevPAR figures show a minor decline in comparison to the previous year, mainly driven by a lower average rate performance, while occupancy increased only marginally.

- When comparing year-to-August 2024 to the same period in 2019, RevPAR is significantly higher, mainly driven by the significant increase in average rate since then.

Hotel Supply

COVID-19 put the London hotel market on hold for two years, but the recovery of the industry proved its resilience. As of September 2024, London has 1,570 hotels providing 145,984 rooms, with more than 36% of the supply being four-star hotels, followed by budget hotels at almost 20% of the total supply. Since 2016, hotel supply in London has grown at a broadly equal compound annual rate across all hotel categories, with the exception of two-star hotels and hostels, which recorded declining room numbers over that period. Over the past year, there have been numerous new openings, including the 57-room Broadwick Soho, the 190-room Peninsula London, the 120-room Raffles London, the 109-room Hampton by Hilton Old Street and the 50-room Mandarin Oriental Mayfair.

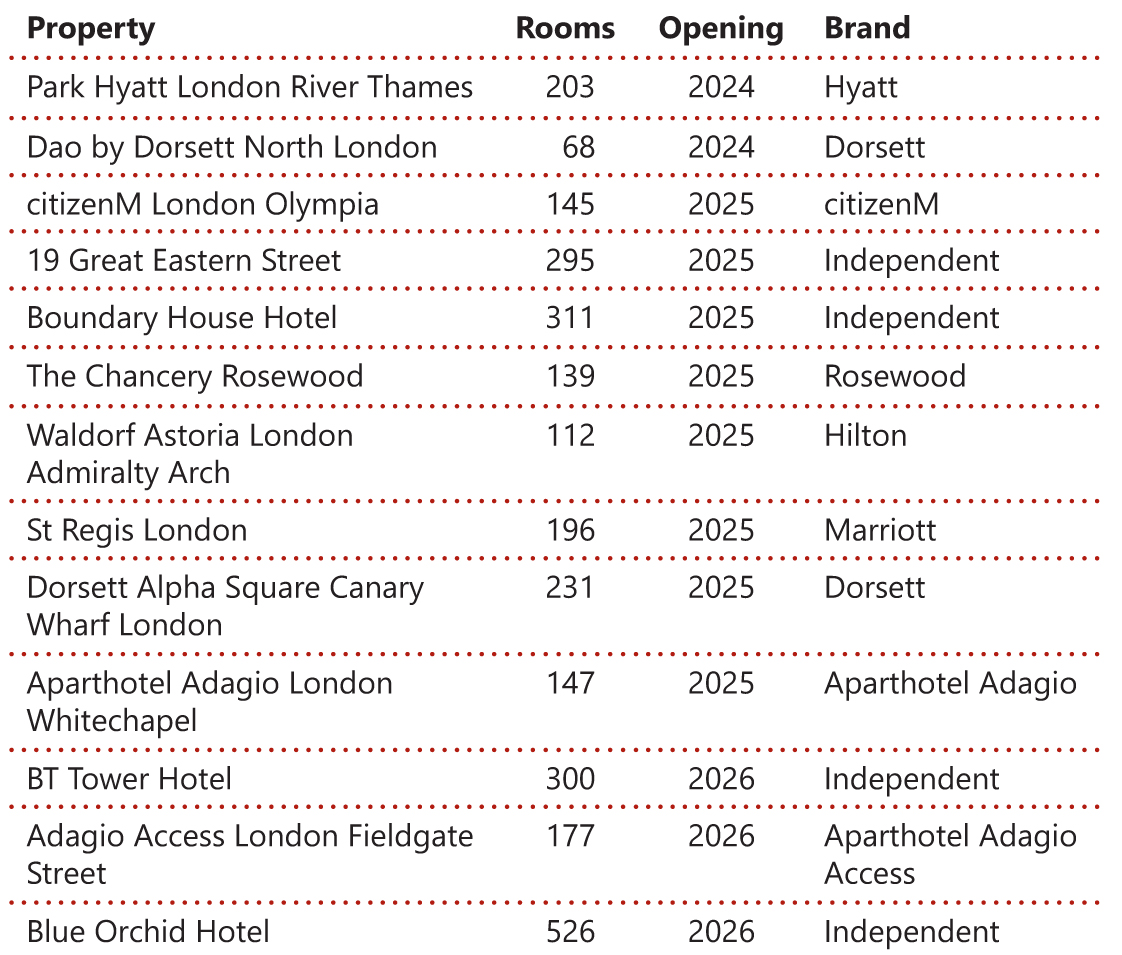

London has a pipeline of 86 hotels scheduled to open between 2024 and 2026, totalling 11,155 rooms. There is particular momentum for independent hotels, which account for 60% of the pipeline. On the branded side, Park Hyatt expects two projects to open by the end of 2024 and hub by Premier Inn counts six projects across the city. The extended-service industry seems to be on the rise, as two Adagio Aparthotel projects are in the pipeline. We also note the ambitious project of turning the landmark BT Tower into an independent hotel, planned to open in 2026.

Hotel Pipeline

Source: HVS Research

Investment Market

London’s hotel investment market showed resilience after the COVID-19 pandemic, with transaction volume rebounding in 2021 and a particularly strong performance in the second quarter of 2022. After a slight slowing down in activity from Q3 2022, the last quarter of 2023 recorded significant growth in transaction volume, mostly owing to the sale of two Hoxton properties for approximately £215 million. In 2023, the average price per key remained relatively on par with pre-pandemic levels, with a wide range of around £85,000 to £600,000 per key. 2024 recorded a very strong start, with the sale of a portfolio of ten Radisson Blu properties in January for a total of around £800 million and the Starwood Aparthotel Portfolio among the other notable transactions. Some of the recent key transactions are shown in the table below.

Hotel Transactions

Source: HVS Research

Outlook

As key performance indicators (average rate, occupancy and RevPAR) continue to demonstrate improvement, the forecast for London’s hospitality industry remains positive. With significant transaction activity and a strong pipeline, the market inspires confidence among key players in the hospitality industry and attracts both investors and travellers. Moreover, a decline in inflation is expected to bolster purchasing power, benefitting the tourism industry. With London having resumed its hosting of a range of popular events at full capacity again and with significant events generating demand in 2025, such as the London Marathon (April), Wimbledon (July), and Coldplay and Oasis concerts (July, August and September), the outlook for the city is positive.

Value Trends 2023 vs 2022

Source: HVS Research

About Cassandre Pene

About Luisa Russell

0 Comments

Success

It will be displayed once approved by an administrator.

Thank you.

Error