Recent metrics for the Minneapolis-St. Paul hotel market illustrate a positive trend. By year-end 2023, hotel occupancy in the Twin Cities rebounded to approximately 57%, according to STR. Data through September 2024 reflect a 6.3% gain in RevPAR over the same period last year due to a slow but steady increase in leisure, group, and corporate travel, coupled with moderate rate growth and declining inventory. While the metro area’s year-to-date growth greatly outpaced that of the nation, the market metrics remain significantly below the national levels, partially due to the limited return to offices and corporate travel volume, as well as new supply that opened prior to and during the pandemic.

Recent metrics for the Minneapolis-St. Paul hotel market illustrate a positive trend. By year-end 2023, hotel occupancy in the Twin Cities rebounded to approximately 57%, according to STR. Data through September 2024 reflect a 6.3% gain in RevPAR over the same period last year due to a slow but steady increase in leisure, group, and corporate travel, coupled with moderate rate growth and declining inventory. While the metro area’s year-to-date growth greatly outpaced that of the nation, the market metrics remain significantly below the national levels, partially due to the limited return to offices and corporate travel volume, as well as new supply that opened prior to and during the pandemic.Fortunately, conventions, sporting events, and festivals have offset the loss of this business and have contributed to the year-to-date resurgence. Major venues, such as U.S. Bank Stadium, Xcel Energy Center, Mall of America, and the Minneapolis Convention Center, continue to attract significant crowds, boosting the demand for nearby lodging facilities.

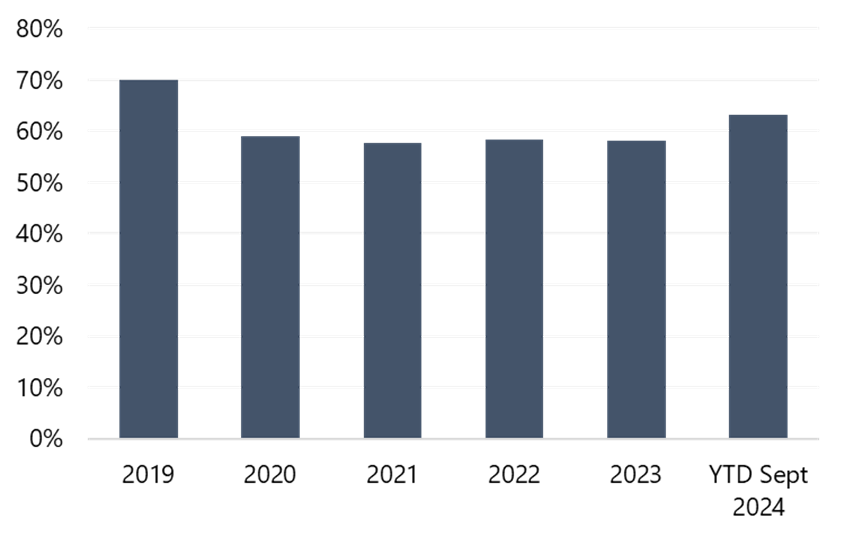

While Minneapolis-St. Paul’s RevPAR has historically registered below the average of the top 25 markets, the metro area suffered heavier losses during the pandemic and has been slower to recover. However, modest demand growth and strong ADR have fueled some improvement in RevPAR through September 2024, registering 63% penetration when compared to the top 25 markets, according to STR.

Minneapolis-St. Paul RevPAR Penetration Compared to Top 25 Markets

Certain submarkets within the Twin Cities are performing better than the rest of the market due to the appeal of the area and/or the diverse base of demand. For example, Bloomington has experienced a favorable rebound given the leisure draw of the Mall of America and proximity of the airport, while the North Loop is a favored locale given the plethora of unique retail and upscale restaurants and new commercial development. Strong demand generated by the Minneapolis Convention Center in 2024 has also fueled the improvement in downtown occupancy, while concerts and special events hosted at the Xcel Center have driven visitation to Downtown St. Paul.

Economic Landscape

The Twin Cities’ economy is fueled by many national headquarters focused on health care, finance, technology, and retail. As of Q3 2024, the unemployment rate in the Twin Cities was slightly lower than the national average; however, market reports detail an office vacancy above 20% in the metro area, with numerous high-profile buildings available for sale or lease amid ongoing negative space absorption.National sports franchises in the metro area include the Minnesota Vikings (NFL), Minnesota Twins (MLB), Minnesota Timberwolves (NBA), Minnesota Lynx (WNBA), Minnesota Wild (NHL), and Minnesota United FC (MLS). In 2024, the venues for these professional teams were highly sought after for other national sporting events, such as the NCAA Big Ten Championships, U.S. Olympic Trials, and NCAA Men’s Frozen Four, with additional events planned in the next several years. The recent success of some of the professional teams has generated additional room nights and provided positive publicity for the Twin Cities.

Investment Opportunities and Outlook

As the Twin Cities hotel market shows stronger signs of recovery in 2024, opportunities for investment abound, with a significant number of hotels currently being marketed for sale. Limited new supply on the horizon, coupled with growing ADR and a gradual return to offices, is expected to lead to favorable upside for investors coming into the market. Many of the assets available for sale need renovations, but as financing becomes more affordable, properties located near key attractions and demand generators are becoming particularly appealing.Many operators have taken advantage of the slower occupancy period to renovate and reposition their properties. Numerous metro-area hotels changed franchise affiliations in 2024, including the DoubleTree by Hilton Minneapolis Airport, the Lofton Hotel Tapestry Collection Minneapolis, the Holiday Inn Express Eden Prairie, and the Wyndham Mall of America, to name a few. Furthermore, some investors have elected to discontinue their affiliation and operate independent of a brand, while others have repurposed their hotels into other uses.

Occupancy in the year-to-date 2024 period remained 10% below the 2019 level; however, the new high-rated supply and robust leisure demand have buoyed ADR in the market, raising the market rate ceiling. Market ADR eclipsed the 2019 level in 2022, aiding in the recovery of RevPAR. As of September 2024, STR reported that Minneapolis-St. Paul hotels achieved a RevPAR slightly above pre-pandemic levels, which is an encouraging sign for a market still seeking to recoup lost corporate demand and attract new groups to the Minneapolis Convention Center and Saint Paul RiverCentre. Thus, as local corporations continue to revise their in-office policies and bolster corporate demand, occupancy should grow.

Twin Cities hotels have yet to recover to the annual occupancy levels realized pre-pandemic, and it is unlikely that occupancy will return to these levels given the more limited corporate travel coupled with the supply growth prior to and during the pandemic. However, the quality of the newer supply and improvements and repositioning of the existing inventory should bolster rate increases, resulting in continued above-average gains in RevPAR.

To learn more about the Minneapolis-St. Paul hotel market or for help making informed investment decisions that align with your goals and risk tolerance, please contact Tanya Pierson, MAI.

About Tanya J. Pierson, MAI

Really interesting. Similar things in Boston, with respect to business travel and a shift in market mix. It used to be evenly divided in thirds, here, across commercial, leisure, and group. Now it's 40/40/20. You have to wonder if this hole in the donut isn't permanent.